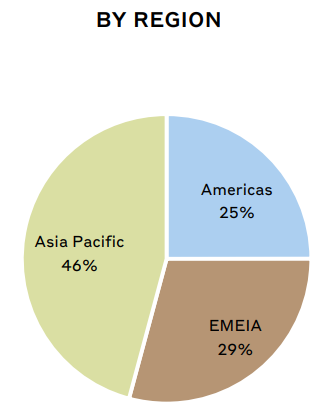

Far behind French behemoths such as Louis Vuitton, Chanel or Hermès, Burberry is nevertheless the tenth largest brand in the world in the luxury sector. However, Burberry's sales have not kept pace with its competitors. Like all luxury giants, it has focused on Asia Pacific, where high-end products sell very well. The region accounts for 46% of sales (57.4% for Hermès, in comparison). The reopening of China is good news, while South Korea, Japan and Hong Kong are dynamic areas. Other Asian markets, such as Thailand, are gaining momentum and offering new growth drivers for luxury goods.

The Americas account for 25% of revenues. The high-end clientele in the major cities is supporting growth. Finally, the large zone that encompasses Africa, the Middle East and Europe, which is abbreviated to EMEA, represents 29% of revenues. Tourists are the main asset of this region.

Breakdown of sales by region (source: Burberry

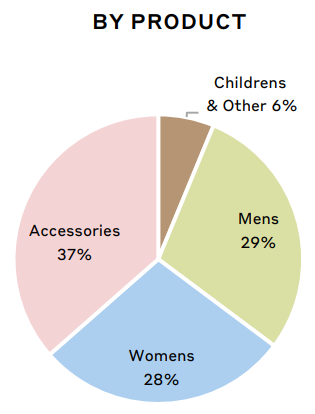

When people think of Burberry, they usually think of the Trench Coat. This large belted raincoat has made the British brand famous. Clothing sales represent about 63% of the turnover (29% for men and 28% for women and 6% for children). The remaining part is represented by accessories such as caps, belts, wallets, scarves, umbrellas, glasses, socks, ties, etc

.

Breakdown of sales by product (source: Burberry)

New with old

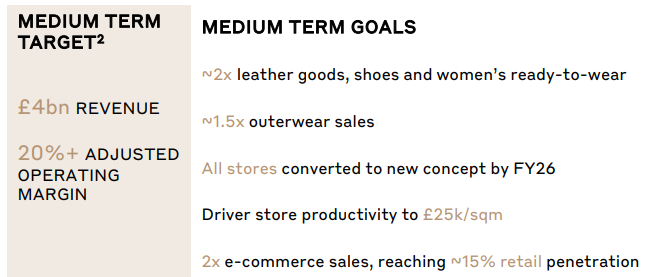

As I mentioned earlier, the company has faced difficulties in the past few years: low growth, stock price going up and down, aging stores and products. So it decided to make changes. The management team was updated for the most part between 2017 and 2018. Between 2018 and 2021, the new management focused on redefining the brand image, moving the leather goods upmarket, and getting back up to speed with the competition. With that done, 2022 is the starting point for a new phase: Redesigning stores to increase their productivity by 15% (the latter represent 80% of sales), refocusing the firm on its historic British character, seizing the opportunity of e-commerce with the goal of doubling online sales to 15% of the total in the medium term and 20% in the long term and increasing accessories to 50% of total sales.

Medium-term objectives (source: Burberry)

Enough to boost the group whose 2022 sales (£2.83 billion) are only slightly above those of 2017 (£2.77 billion). The operating margin has not returned to its 2013/2014 level. At that time it was around 20% and at the end of 2022 it stood at 18.5%. While waiting to see the merits of the new strategy, Burberry still has a few tricks up its trench coat's sleeve.

(Overly?) pampered shareholders

Over the period 2013-2022, the free cash flow amounted to £3.31 billion. A very large part of this was used to remunerate shareholders through dividends and share buybacks. The number of shares thus fell from 438.1 million in 2013 to 376.5 million last year, a reduction of 16.4% in less than 10 years. As for the dividend, it has been stable over the period, offering an average yield of 2.2%. This is perhaps a sign of the fragility of the brand, which is unable to increase its results and pay out a dividend that increases year on year like its French competitors. The allocation of capital has certainly not been the most strategic.

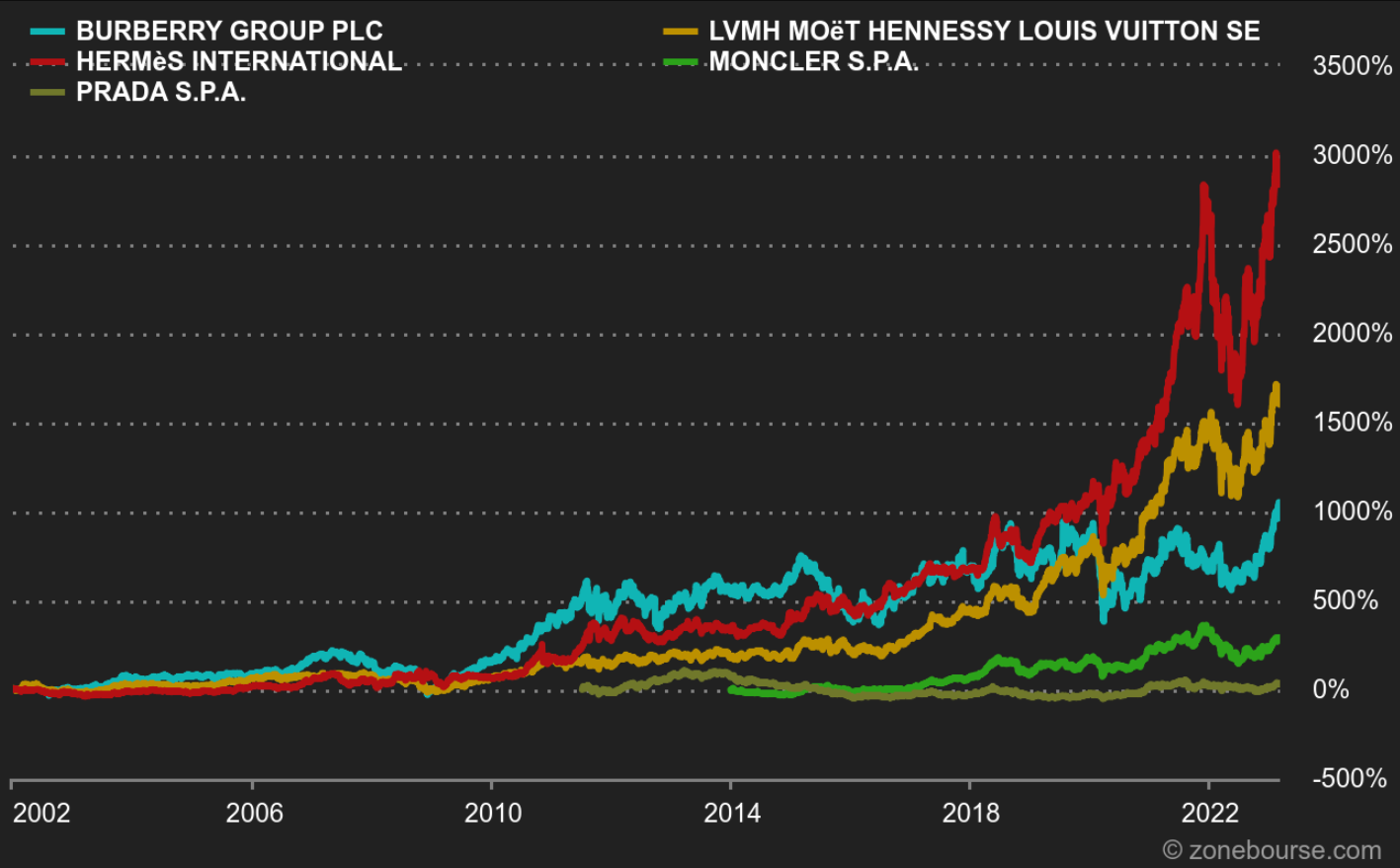

However, it has had the advantage of supporting the share price and increasing it to high levels: since 2002, the share price has increased more than tenfold, from around £230 to £2500. Since 2013, and to take the previous analysis period, the share price has doubled despite strong fluctuations. However, the performance remains mediocre compared to the champions of the sector.

Evolution of the prices of luxury competitors (source: MarketScreener)

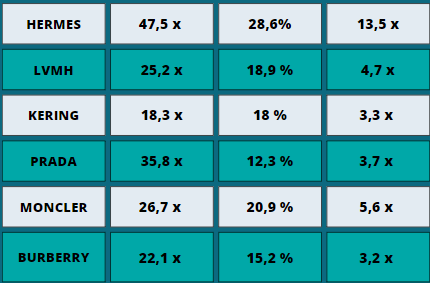

The valuation is lower than the competitors. The stock is paying 22.1 times its 2023 profits when all ultra luxury competitors have a higher valuation (except Kering, whose difficulties with Gucci continue to weigh on the company). The net margin is well below the other behemoths and in this respect, Burberry is only ahead of Prada. Note that Prada is a special case, and is the subject of many rumors including a potential listing in Europe (the stock is listed in Hong Kong).

How Burberry compares to its competitors for the fiscal year 2023 (PER - Net margin - Capitalization/Turnover)

Burberry may have been thinking too much about its shareholders - which is not necessarily a bad thing - but it neglected new growth investments. The new phase of the strategic plan, started last year, is supposed to boost growth to bring the best representative of British luxury closer to its French and Italian competitors.